minervaimn9739

About minervaimn9739

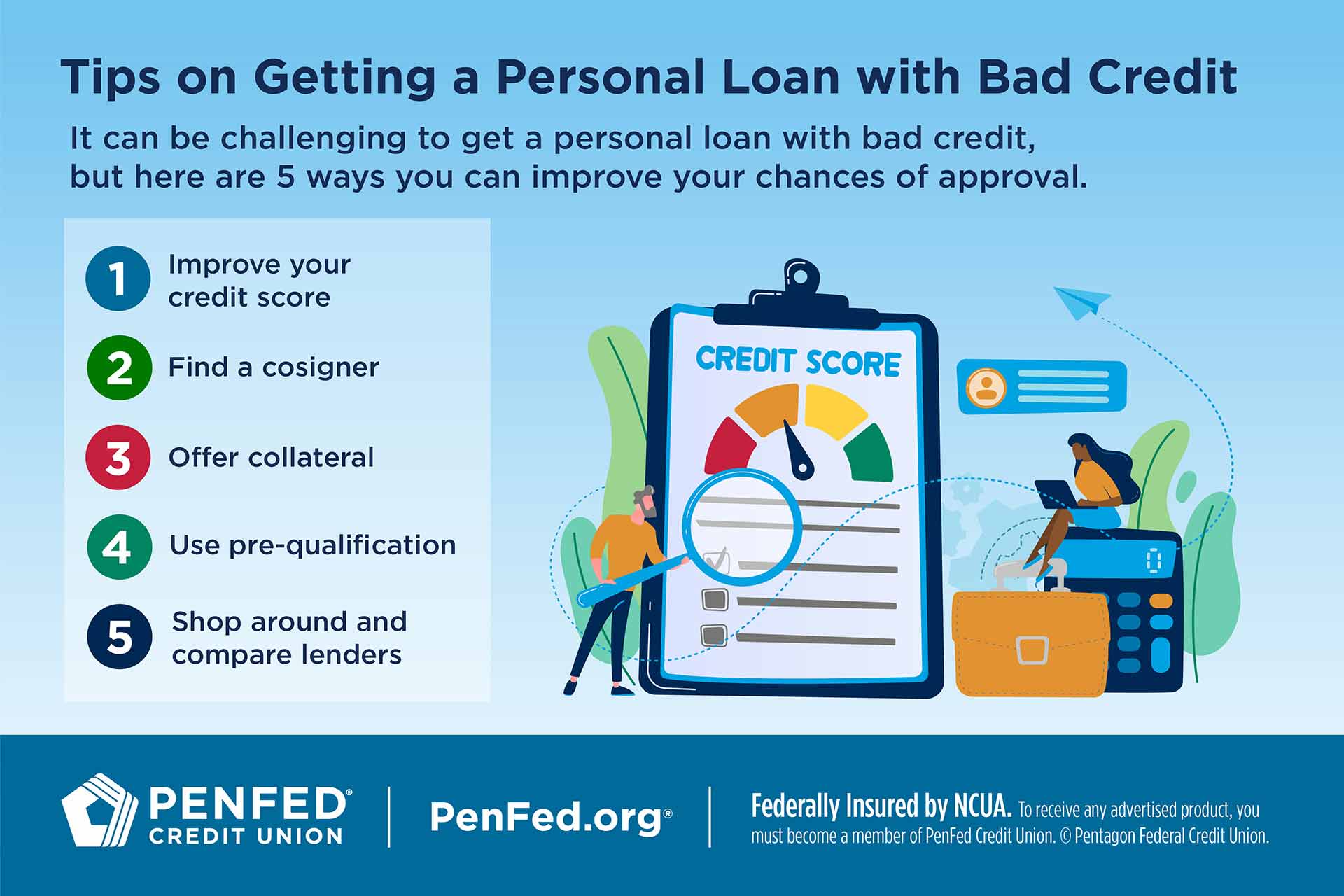

Understanding Personal Loans For Bad Credit: A Case Examine

In today’s monetary landscape, personal loans supply people the opportunity to secure funds for numerous functions, from consolidating debt to financing a home renovation. Nonetheless, for these with dangerous credit, accessing these loans can be a daunting problem. This case study explores the journey of an individual with unhealthy credit score seeking a personal loan, examining the obstacles confronted, the options available, and the classes realized throughout the method.

Background

Meet Sarah, a 32-yr-previous single mother living in a suburban area. After a collection of financial setbacks, together with medical payments and unemployment, Sarah found herself with a credit score rating of 580, which is taken into account poor. Despite her efforts to handle her finances responsibly, her credit score historical past reflected late payments and high credit score utilization. Sarah needed a personal loan of $10,000 to consolidate her current debt and make obligatory residence repairs.

The Problem of Bad Credit

When Sarah first approached her bank for a personal loan, she was met with disappointment. The financial institution’s stringent lending standards, which included a minimal credit rating of 650, meant that she was automatically disqualified. Annoyed however determined, Sarah started researching alternative lending choices.

Exploring Alternate options

Sarah found that there are several forms of lenders that cater to individuals with bad credit score. These included credit score unions, online lenders, and peer-to-peer lending platforms. Every option got here with its own set of pros and cons:

- Credit score Unions: Sarah discovered that credit score unions typically have more flexible lending standards in comparison with traditional banks. If you have any concerns concerning where by and how to use quick personal loans for bad credit, you can speak to us at our web site. She utilized for a loan at her native credit union, which required her to turn out to be a member. Though the interest charges have been slightly lower than these provided by on-line lenders, the application course of took longer than anticipated, and her loan was in the end denied on account of her credit score score.

- On-line Lenders: Subsequent, Sarah turned to on-line lenders. Many of these lenders specialize in personal loans for individuals with bad credit. After comparing a number of choices, she utilized for a loan with a good online lender that marketed loans for those with credit score scores as little as 550. The application course of was straightforward, and she acquired a conditional approval within minutes. Nonetheless, the interest charge was considerably increased, at 25%, and the fees have been substantial.

- Peer-to-Peer Lending: Sarah additionally explored peer-to-peer lending platforms, the place people can lend cash to others immediately. She created a profile and shared her story, hoping to draw potential lenders. While she obtained several affords, the curiosity charges diverse widely, and she was uncomfortable with the concept of borrowing from particular person investors who may not have her finest pursuits in mind.

The choice-Making Process

After much deliberation, Sarah decided to simply accept the supply from the online lender, despite the excessive curiosity charge. She realized that consolidating her debt would in the end help her enhance her credit score score, making it simpler to secure better loan phrases in the future. The lender granted her the loan, and she used the funds to repay her high-interest credit score playing cards and make essential repairs to her dwelling.

The Influence of the Loan

With the personal loan secured, Sarah was capable of consolidate her debt right into a single month-to-month cost, which was considerably lower than what she had been paying earlier than. This not solely eased her financial burden but additionally allowed her to focus on rebuilding her credit score. Over the following few months, she made constant funds on her loan, and as her credit score utilization ratio improved, her credit rating started to rise.

Classes Learned

Throughout her expertise, Sarah realized several necessary classes about acquiring personal loans with unhealthy credit score:

- Analysis is vital: Sarah discovered the significance of researching completely different lenders and understanding the terms of each loan. By evaluating choices, she was able to discover a loan that met her needs, even if it got here with higher interest charges.

- Credit Unions Could be Helpful: While her expertise with the credit score union was finally unsuccessful, Sarah recognized that credit score unions often present extra personalized service and should provide decrease charges for members. She plans to proceed constructing her relationship together with her local credit score union for future monetary wants.

- Bettering Credit Takes Time: Sarah learned that rebuilding her credit score would take time and constant effort. She started budgeting more successfully, paying bills on time, and avoiding new debt, which contributed to her monetary recovery.

- Consider Financial Counseling: After her expertise, Sarah realized the value of financial counseling. She sought recommendation from a non-profit credit score counseling service, which helped her create a plan to handle her funds and enhance her credit score score further.

- Avoid Predatory Lending: Sarah encountered gives from lenders with predatory practices, comparable to exorbitant charges and interest rates. She discovered to acknowledge warning indicators and to be cautious about affords that seemed too good to be true.

Conclusion

Sarah’s journey to safe a personal loan regardless of her unhealthy credit highlights the challenges faced by many people in related conditions. Whereas the road was fraught with obstacles, her determination and willingness to explore totally different options in the end led to a positive end result. By understanding the lending landscape, making informed choices, and committing to enhancing her credit, Sarah is now on a path toward financial stability and empowerment. This case research serves as a reminder that whereas dangerous credit can complicate the borrowing course of, it is not an insurmountable barrier to reaching monetary goals.

No listing found.